According to the new market research report ” Bioinformatics Market by Product & Service (Knowledge Management Tools, Data Analysis Platforms (Structural & Functional), Services), Applications (Genomics, Proteomics & Metabolomics), & Sectors (Medical, Academics, Agriculture)”, global bioinformatics market is expected to account for USD 7,063.7 billion in 2018. It is expected to reach USD 13,901.5 billion by 2023, at a CAGR of 14.5% during the forecast period.

Growth of the bioinformatics market is driven by the growing demand for nucleic acid and protein sequencing, increasing government initiatives and funding, and increasing use of bioinformatics in drug discovery and biomarker development processes. With the introduction of upcoming technologies such as nanopore sequencing (third generation sequencing technique) and cloud computing, the market is expected to offer significant opportunities for manufacturers of bioinformatics solutions.

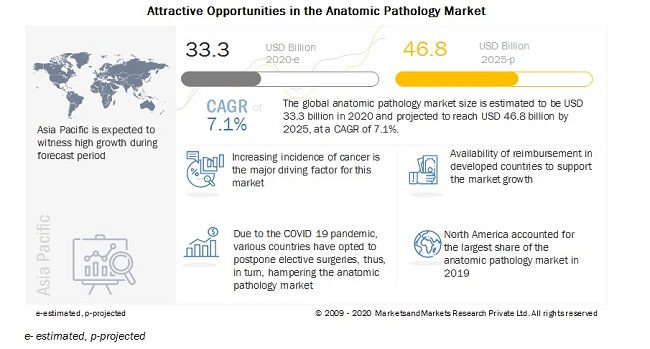

Expected Revenue Growth:

[195 Pages Report] The global bioinformatics market is expected to account for USD 7,063.7 billion in 2018. It is expected to reach USD 13,901.5 billion by 2023, at a CAGR of 14.5% during the forecast period.

Accessories to Fuel the Growth of Bioinformatics Market :

Bioinformatics is the application of computer technology for the management and analysis of biological data. It includes collection, storage, retrieval, manipulation, and modelling of data for analysis, visualization, or prediction through algorithms and software.

However, factors such as a dearth of skilled personnel to ensure proper use of bioinformatics tools and lack of integration of a wide variety of data generated through various bioinformatics platforms are hindering market growth.

Browse in-depth TOC on “Bioinformatics Market”

189 – Tables27 – Figures195 – Pages

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=39

By Application, the metabolomics segment is expected to grow at the highest CAGR during the forecast period

Factors such as the availability of research funding and government support are fueling market growth. However, metabolomes cannot be easily identified or figured from reconstructed biochemical pathways due to enzymatic diversity, substrate ambiguity, and difference in regulatory mechanisms. Hence, the annotation of unknown metabolic signals is the main hindrance to growth of the metabolomics segment.

In 2018, The APAC market is expected to grow at the highest CAGR during the forecast period

The market in the Asia Pacific region is expected to offer significant opportunities for players to offset revenue losses incurred in mature markets. Emerging countries in this region are witnessing growth in their GDPs and a significant rise in disposable income levels. This has led to increased healthcare spending by a larger population base, healthcare infrastructure modernization, and rising penetration of cutting-edge research and clinical laboratory technologies, including bioinformatics, in Asia Pacific countries. These factors are expected to provide significant growth opportunities to bioinformatics companies operating in this region.

Request Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=39

Key Market Players

Thermo Fisher Scientific, Eurofins Scientific, Illumina, Perkinelmer, Inc., Qiagen Bioinformatics, Agilent Technologies, Dnastar, Waters Corporation, Sophia Genetics, Partek, Biomax Informatics AG, Wuxi Nextcode, Beijing Genomics Institute (BGI)